I don't have much to add. My thoughts on today's action are that the bond is playing catch up to all the negative rate news. Lets see it was Greenspan, PPI, S. Korea, and new commodity highs with the long bond still yielding 4.64% this morning. I don't see anything in particular that drove the action today.

Stocks are left sorting out what is going on in the world and whether we will see stagflation or inflation.

Feb 28, 2005

Japanese Industrial Production Tops Forecast

Bloomberg:

The yen rose in Asia, the biggest fluctuation of any major currency market today, after Japan's government said industrial production grew more than forecast, helping the world's second-largest economy recover from recession.

The biggest increase in production since April and a separate report showing the first gain in retail sales in three months helped the yen rise the most of 16 other most-traded currencies today. The yen is up 4.2 percent against the dollar in the last six months as overseas investors put money into Japanese stocks.

The reports ``are further confirmation that the economy has bottomed out and is recovering,'' said Naomi Fink, a currency strategist in Tokyo at BNP Paribas SA

Feb 27, 2005

The Growing Power of Asian Central Bankers

The FT($$) writes:

If you just can't read enough about the U.S. dependence of Asian central banks, you can check out the China Stock blog's summary of a Barron's article. The gist of the article is that China's peg is not so bad. One argument they make is that a yuan appreciation is not a given in a free market because all emerging market currencies are undervalued based on purchasing power. I think you could drive a large truck between the yuan's current value and "undervalued based on purchasing power" but a more thorough approach is to compare values across emerging economies. I have not read the Barron's article but the summary was food for thought.

So why should we pay so much attention to the six leading central bank governors in Asia? Quite simply because if any one of them decided to diversify his country's exchange reserves aggressively out of dollars, the kind of currency market jitters we saw this week would pale into insignificance. Furthermore, if Asian central banks merely decide to follow South Korea in ceasing to buy new US assets, economists estimate that the interest rate on long-dated treasuries could rise by 0.4 to 2 percentage points.

In short, one of the main drivers of monetary conditions in the US is the Asian central banker.

This is the point I was making in my dialogue with Roger. It remains to be seen if the Fed still has the same flexibility to act in a crisis but my guess is that they don't. This will be especially true if the crisis begins in the U.S., limiting the a flight to quality response the U.S. bond market normally sees.

If you just can't read enough about the U.S. dependence of Asian central banks, you can check out the China Stock blog's summary of a Barron's article. The gist of the article is that China's peg is not so bad. One argument they make is that a yuan appreciation is not a given in a free market because all emerging market currencies are undervalued based on purchasing power. I think you could drive a large truck between the yuan's current value and "undervalued based on purchasing power" but a more thorough approach is to compare values across emerging economies. I have not read the Barron's article but the summary was food for thought.

Feb 26, 2005

Couple of Dollar Thoughts

I thought this story about S. Korean diversification was interesting.

I also hopped in a thread on Macroblog about whether the adjustments made by foreign central banks will necessarily cause shocks. I tend to think at least some markets will experience sharp movements. U.S. interest rates and the dollar seem like likely candidates. Obviously the CBs will target gradual adjustments but it remains to be seen if markets will go along.

A South Korean parliamentary committee passed a bill Friday that will allow the nation to use part of its massive foreign reserves for overseas investment.I have only seen this story from one source which I find a bit strange but if true it emphasizes that diversification refers to asset class rather than currency. That is a completely different ballgame from Tuesday's story though I imagine their actions will come somewhere in the middle. Reduced purchases of both U.S. debt and the dollar make sense. This asset diversification is what I referred to last week and will lead to higher U.S. interest rates but possibly a very positive medium-term reaction in other markets.

The move is part of the country's long-term plans to diversify more than $200 billion of foreign reserves, Finance Ministry officials said.

Under the bill endorsed at the National Assembly committee on finance and economy, the government can use 10 percent of its foreign reserves for investment in stocks and real estate in foreign nations.

I also hopped in a thread on Macroblog about whether the adjustments made by foreign central banks will necessarily cause shocks. I tend to think at least some markets will experience sharp movements. U.S. interest rates and the dollar seem like likely candidates. Obviously the CBs will target gradual adjustments but it remains to be seen if markets will go along.

Equity Market Thoughts

The one thing I keep thinking about yesterday's stock market action is that it was really a mirror image of Tuesday's selling. It does have the advantage of taking place near multi-year highs though. Yesterday also had the familiar weak dollar - strong commodities - strong stocks - lower yield pattern that has been the hallmark of the bull market since Spring '03.

To really gain my confidence I would prefer seeing the market prove it can move up with yields. Might not matter for the short run with all the open gaps in the bond chart below current yields but eventually it seems like a necessity for higher stock prices.

To really gain my confidence I would prefer seeing the market prove it can move up with yields. Might not matter for the short run with all the open gaps in the bond chart below current yields but eventually it seems like a necessity for higher stock prices.

Feb 25, 2005

Bill Gross Analyzes the Conundrum

This is part of his conclusion about the strange times we live in.

His chart of U.S. debt outstanding against domestic ownership is just plain scary.

In light of our rationale, which attempts to explain the great "conundrum," an interested reader might wonder why our durations and overall strategy appear so defensive. After all, if foreign central banks and others continue to absorb 70%+ of the bond market's new supply (900 billion out of an estimated 1.3 trillion in 2004), why wouldn't this "squeezing" out of domestic investors continue unabated, with yields continuing to move lower? The insensitivity to price/yield exhibited by Asian central banks in an effort to cap their own currencies might seem just as illogical 50 basis points lower as it does right now. And if the lack of global aggregate demand reflected in a surfeit of savings is really the primary cause, the malady is not likely to improve for years. Point granted. We might be at the mercy of a bond market tsunami here, whose first wave has struck and is now receding, only to be followed by more of the same in a few short months. This possibility is part of any interest rate guessing game except it is complicated in this new instance by buyers who have non-interest rate concerns. Still, there are limits. Why would a central bank buy 10-year Treasury paper below 4% if it expected 3-month Treasury Bills to be yielding 3 1/2% by the end of the year? It could cap its currency just as easily by going the short maturity route without risking future price losses. And for those institutional foreign bond holders, and the "hedgies" domiciled in the Caymans, there's no doubt too that a higher and higher short rate reduces and in some cases eliminates "carry," leading to collapsed positions and ultimately higher yields further out on the curve.The interesting aspect was his wait and see approach. He knows how it will end but does not see when that end will arrive and is making sure he can out last the central banks. The system does not seem sustainable for long in my view but it is easy to see that surviving to pick up the pieces is a pretty attractive option.

His chart of U.S. debt outstanding against domestic ownership is just plain scary.

Squeezy

The action feels like it is being squeezed higher today. I am a bit surpised so many shorts would get in on Tuesday's selloff and would guess quite a few were in near last weeks highs. This can probably continue into next week but ultimately I think the best long entries will come below yesterday's lows.

The chatter (and prices) in oil and commodities is a touch frothy and I am not sure it can continue much longer. The falling bond yields do not confirm the higher commodity prices so that could be a sign to book some profits. I prefer owning the precious metals over the industrials as they have been left behind a bit.

The chatter (and prices) in oil and commodities is a touch frothy and I am not sure it can continue much longer. The falling bond yields do not confirm the higher commodity prices so that could be a sign to book some profits. I prefer owning the precious metals over the industrials as they have been left behind a bit.

China Plods Forward

China Economic Net sourced this from the People's Daily but I could not find it there.

China will speed up the infrastructure construction of foreign exchange market, increase varieties of transaction in the inter-bank forex market and experiment on US dollar market maker system. It means China is expected to introduce the US dollar market maker system into its foreign exchange management system.It is probably not news because its sounds mostly like a technical change but markets might take notice.

Closing Time

Today's morning anxiety eventually gave way to a pretty nice run. It should hold up for tomorrow but I would be a bit surprised if we held this morning's lows through next week. Breadth was strong today but the move lacked volume. Would have been a much better bottom if sellers had gotten stopped cold in the morning rather than everyone just waiting until noon to start playing. As it stands interest is still focused in commodity related stocks and housing. There is no lack of volume in TOL or X.

A couple of charts I follow look like they are in a good position to move up here. They are HAE and NEOL. I probably won't be adding any long-term positions though and may stick to day trading for a bit. The market seems to be trading as a unit reacting to bonds and oil and while that goes on the risk seems higher. I usually see things better when I am flatter and market is still figuring out which way the trend will be. Less so for bonds and commodities I think but the dollar rally tonight might mix that up a bit too.

I was surprised by how much the VIX fall off today. The market got a bit ahead of itself this week but I am not sure I would be bailing out of my insurance just yet. Makes me wonder a bit if people have too much premium at risk for the large percentage swings in volatility. I wonder if it is creating overtrading at a good long-term entry level.

A couple of charts I follow look like they are in a good position to move up here. They are HAE and NEOL. I probably won't be adding any long-term positions though and may stick to day trading for a bit. The market seems to be trading as a unit reacting to bonds and oil and while that goes on the risk seems higher. I usually see things better when I am flatter and market is still figuring out which way the trend will be. Less so for bonds and commodities I think but the dollar rally tonight might mix that up a bit too.

I was surprised by how much the VIX fall off today. The market got a bit ahead of itself this week but I am not sure I would be bailing out of my insurance just yet. Makes me wonder a bit if people have too much premium at risk for the large percentage swings in volatility. I wonder if it is creating overtrading at a good long-term entry level.

Inflation Targets and Asset Bubbles

From the Economist:

I am getting a bit out of my area of expertise but I am pretty sure the Fed (and probably the world) is running into the problem the Economist describes with asset prices demonstrating large value swings while goods prices remain stable. These swings are making it impossible to effectively manage liquidity in the system. Rather than giving central banks the difficult task of adjust policy to correct asset prices I think it is better to create a mechanism for asset price stability outside of central bank control.

Some central bankers in Britain, continental Europe, Australia and New Zealand have said publicly that monetary policy needs to take more account of asset prices and that sometimes interest rates may need to rise by more than if the sole objective were to keep consumer-price inflation within target.The author then gets a bit caustic with the Fed for reluctance to consider the overall liquidity picture and concludes with this.

During the past century, every monetary rule has eventually broken down: the gold standard, the Bretton Woods system of fixed exchange rates, and monetary targeting. Now it seems that strict inflation targeting may not be a panacea either. It would be foolish for the Fed to sign up for crude inflation targeting just as it goes out of fashion.While centering on the need to include asset prices in inflation measures the article falls a bit short by suggesting central banks should consider asset prices in their policy decisions. A better solution is to remove asset prices from central bank control. Robert Shiller discusses the Chilean UF (unit of development) in his book The New Financial Order (Amazon) as an example of an alternative system to limit central bank influence over asset prices. The UF is an inflation indexed unit of account which is repriced daily such that everyone knows the correct price of a UF in Pesos. The UF was created in 1967 and has become widely used for pricing long-term contracts such as housing prices and mortgages while pesos are still used for day-to-day purchases and salaries.

I am getting a bit out of my area of expertise but I am pretty sure the Fed (and probably the world) is running into the problem the Economist describes with asset prices demonstrating large value swings while goods prices remain stable. These swings are making it impossible to effectively manage liquidity in the system. Rather than giving central banks the difficult task of adjust policy to correct asset prices I think it is better to create a mechanism for asset price stability outside of central bank control.

Feb 24, 2005

Dollar Counterpoint

I have written and passed on quite a bit of dollar/ U.S. debt/ Asian lending news lately. Not to be a panic monger there is a still a good possibility for an anti-climactic resolution. There are probably many ways this could occur but General Glut lays out what I see as the most likely other alternative to a weakening dollar that pressures central bank UST holdings creating a downward spiral.

Second, it may be that the East Asians do not convert their dollars into local currency and suffer high capital losses. China in particular does not fully sterilize and thus is not issuing as much local currency debt to soak up inflowing dollars. Japan doesn't sterilize at all. Both countries could use central bank dollars to loan to private firms looking to make investments in/purchases of oil (still priced in dollars), US corporations, US mineral deposits, US agricultural land, US golf courses, whatever. We already know that all the East Asian banks have accumulated reserves far in excess of what they "need" to defend their currencies. So why not simply keep many of those dollars in dollar form and buy US real assets with them?As always the entire post is worth reading but this paragraph is really the heart of things in my view. It is possible that Asian central banks simply shift out of bonds into other assets. The kicker here is that it is not a solution to interest rates heading up which may still lead to problems even with a strong dollar. But it would certainly play out differently for stocks and possibly real estate.

Give Green a Chance

FNM has held near the flat line and now migrated positive. The market is up with it. This bounce is mostly about the immediate term negativity in the market. IMHO if FNM makes a new low today the market will put in a very ugly day.

If You Haven't Gotten Your Fill of Dollar Reading

I recommend this entertaining look at the things from Whiskey Bar which I found via Brad Setser's Web Log.

Search Names may have Troubles Too

The story unfolding from FindWhat (FWHT) also looks like trouble for a space with some pretty high multiples.

These posts lay it out pretty good. One, two, three...

These posts lay it out pretty good. One, two, three...

Fannie Mae could be "The Story" Today

The NY Times ran an article that begins with this.

If FNM does get going on the downside keys to how it plays out will be whether the banks follow it down and whether treasuries can manage a pop on a flight to quality. If you get banks and bonds down the dollar will go too and that is when it is a real problem.

The market could focus on the extension but that first paragraph is a bit of a disaster. It sets up the stock to break down from an already oversold condition. That situation could get ugly in a hurry and there is still massive exposure to that name in the bond market.FANNIE MAE, the nation's largest buyer of home mortgages, said on Wednesday that its primary regulator had discovered a host of new potential accounting violations at the company that had raised a fresh set of "safety and soundness concerns."

Fannie Mae also said that regulators had decided to give it a three-month extension, until the end of September, to carry out a plan to raise billions of dollars in capital and reduce its portfolio of mortgage securities.

If FNM does get going on the downside keys to how it plays out will be whether the banks follow it down and whether treasuries can manage a pop on a flight to quality. If you get banks and bonds down the dollar will go too and that is when it is a real problem.

Feb 23, 2005

Cost Push Inflation

Check out this chart that is originally from AngryBear but brought to my attention by General Glut.

I don't think this trend is priced into the bond market. Particularly the lag between the bottom of the Core CPI and the PPI seems to imply that things will get worse before they get better.

I don't think this trend is priced into the bond market. Particularly the lag between the bottom of the Core CPI and the PPI seems to imply that things will get worse before they get better.

Steel Moonshot

The FT($$) explains the recent jump in steel stocks.

Rio Tinto on Wednesday became the second big mining group to lock in a 71.5 per cent price increase for iron ore in negotiations with Nippon Steel, Japan's biggest steelmaker.

The move followed an announcement on Tuesday by Brazil's Companhia Vale do Rio Doce, the world's largest iron ore miner, that it had agreed the same price increase with Nippon Steel as well as JFE Holdings and Kobe Steel, also of Japan, for the year beginning this April.

News of the agreements have driven shares in mining companies such as Rio Tinto and BHP Billiton up to record levels. Steel stocks have fallen, however, reflecting worries that the industry will have to absorb the higher costs rather than pass them on to customers in steel price rises.

But steelmakers outside Japan have stressed that the deals struck by Nippon Steel should not be seen as a guide for other iron ore negotiations, as Japan is a relatively small iron ore consumer.

Rapping with Roger.

Roger Nusbaum and I are having a discussion on his blog. This morning he posted this.

The concerns in the market yesterday don't seem like they can be solved by lower U.S. interest rates.

I don't know how serious this may or may not become but as a quick reminder, bear markets don't usually start with crashes. I would think a crash would be no different if it happens this time around. This is not a prediction but ties in with past writings of relying on logic instead of emotion.To which I replied.

Usually sharp selloffs snap back sooner than people expect, think Asian contagion, Russian Ruble & LTCM and 9/11. That may be worth remembering.

None of your snapback examples occurred while the Fed was hiking rates. The best strategy in each of those cases was short until the Fed cuts and then buy.He then responded at the bottom of this post.

"This time it's different" is a difficult argument to make but the current stance of the Fed and increasing reluctance of central banks to finance U.S. borrowing could be a pretty big impediment to following the same course of action.

I don't have a problem with your point so much as your examples.

You may be right. But if there were some sort of horrible event to cause a crash, wouldn't the fed one way or another act? They can add liquidity and jawbone in addition to lowering rates. I would think the fed would do something, again, in the face of a crisis.So I added to my comments as well.

This time around a catastrophe would need a G3 or G10 response. The Fed would have a tough time convincing foreign creditors to continue lending as rates fell. They are having a tough time keeping foreigner lenders (like Korea) in as it is with no crisis and rising rates priced into the forward market.The U.S. has an unprecdented demand for international funding. By committing to borrow so much the U.S. has in effect given up its ability to manage interest rates counter-cyclically. The current worries in the dollar and long-term interest rates in some ways represent the possibility that creditors force U.S. interest rates to be pro-cycle by demanding higher interest rates from the U.S. when its growth prospects look weak.

While the Fed may want to offer stimulous they also need to avoid a dollar collapse. I don't think a simple rate cut would manage it.

The concerns in the market yesterday don't seem like they can be solved by lower U.S. interest rates.

KLAC a Good Short on Technical Failure

Kla-Tencor's (KLAC) has fallen back below 49. With 49 marking the neckline of an inverse-head-and-shoulders it now becomes a short candidate. Failures of easily recognized short-term patterns tend to be hard and fast so at any rate I don't want to own it in here.

French 50-yr Meets Strong Demand

I mentioned Pimco's interest in European yields and not too surprisingly others saw it the same way.

France became the first Group of Seven industrialised country to issue a 50-year bond in modern times, extending the duration in the market from the 30-year segment.

The size of the issue was increased to EUR 6bn from a targeted EUR 3bn-5bn after investors placed orders worth more than EUR 19bn for the bonds, which will mature in April 2055. The strong demand was initially driven by institutional investors including pension and insurance funds, which need longer-dated assets to match their liabilities from an ageing population.

Korea's Clarification

The most interesting part of the new statements addresses diversification into non-government bonds.

Some of the dollar strength this morning is being attributed to the Korean clarification but it seems more likely it is a response to one-sided trading yesterday that set a near-term low.

However the BoK said in a statement on Wednesday that it was looking to invest more in non-government bonds and that it would not sell current dollar holdings for other currencies.Korea has been adding to reserves at a pretty fast clip so even by limiting the policy change to new investments it will still have a pretty strong impact.

We already know that Korea has battled mightily against won appreciation over the past two years, with the Bank of Korea's foreign reserves growing 27% since January 2004 and a stunning 62% since January 2003. And yet the won continues to rise. In early April 2003 the dollar bought around 1260 won; now it buys less than 1030 won, a nearly 20% appreciation.How the U.S. funds this years borrowing need is really what is on the table.

Some of the dollar strength this morning is being attributed to the Korean clarification but it seems more likely it is a response to one-sided trading yesterday that set a near-term low.

A Day Worth Watching

That was the worst day in the equity market since Aug 6th, 2004 but I don't think the fear level was quite the same. Strange times in equities as pariticipants seem pretty relaxed about moves in either direction. Down does feel easier though.

Commodities are a bit more interesting as these recent rallies have really brought out some table pounders. I would be watching the dollar to see if it makes a quick (5-7 trading days) retest of the Dec lows which could set up a pretty powerful bottoming pattern. That would put the kabosh on commodity trades though it is a few days off and far from a done deal.

I have to wonder if by Thursday we will see some Fed officials trying to clarify Greenspan's remarks on interest rates. A bit tough to take back but I would be surprised if they did not try.

Commodities are a bit more interesting as these recent rallies have really brought out some table pounders. I would be watching the dollar to see if it makes a quick (5-7 trading days) retest of the Dec lows which could set up a pretty powerful bottoming pattern. That would put the kabosh on commodity trades though it is a few days off and far from a done deal.

I have to wonder if by Thursday we will see some Fed officials trying to clarify Greenspan's remarks on interest rates. A bit tough to take back but I would be surprised if they did not try.

Feb 22, 2005

Macro Forces move to the Front Lines

While the long-term charts in the dollar and bonds look like a beginning, the emotion in today's tape feels more like an extreme that marks an end. The move in metals, bonds and the dollar began 7 trading days back so Friday's inflation news and today's Korean rebalancing story (emphasis on the word story) may have been anticipated to a large degree.

Stocks certainly have the more room to fall in here if they want to but if its inflation / dollar / commodity prices freaking people out it seems the long bond carries more risk and will lead the way down. Today seems like the kind of day that will leave volatility higher for a few weeks and ditto for correlations. Stocks will trade as an entity while the market sorts out the bigger picture. A jump in volatily could get ugly and end up lasting more than a few weeks given the low starting point.

I have started watching the 10-yr bund / U.S. bond spread as I anticipate that relationship going through some changes.

Stocks certainly have the more room to fall in here if they want to but if its inflation / dollar / commodity prices freaking people out it seems the long bond carries more risk and will lead the way down. Today seems like the kind of day that will leave volatility higher for a few weeks and ditto for correlations. Stocks will trade as an entity while the market sorts out the bigger picture. A jump in volatily could get ugly and end up lasting more than a few weeks given the low starting point.

I have started watching the 10-yr bund / U.S. bond spread as I anticipate that relationship going through some changes.

South Korea spooks the Currency Markets

A while back, I referred to South Korea as the weakest member of the dollar managing cartel in a comment on Brad Setser's site. If you are wondering why South Korea's hint at a policy change may be a big deal I highly recommend reading his entire post. He and Nouriel Roubini have written some great stuff describing the gamesmanship involved in trying to fix currency levels.

In a nutshell we have been watching for 6 months as smaller counties diversify away from the dollar while China and Japan try to maintain the status quo. As of Q4 S. Korea was also trying to keep its currency static to the dollar. If the comments today are not retracted and are followed by action then S. Korea becomes the biggest small country to abandon the dollar. That could conceivably speed up the selling or increase the share of the U.S. borrowing needs that must be funded by Japan and China.

It is best to think about what is going on in terms of game theory with China and Japan sitting in separate rooms and deciding if they can still support the dollar while doing so means increasing the risk of loss.

In a nutshell we have been watching for 6 months as smaller counties diversify away from the dollar while China and Japan try to maintain the status quo. As of Q4 S. Korea was also trying to keep its currency static to the dollar. If the comments today are not retracted and are followed by action then S. Korea becomes the biggest small country to abandon the dollar. That could conceivably speed up the selling or increase the share of the U.S. borrowing needs that must be funded by Japan and China.

It is best to think about what is going on in terms of game theory with China and Japan sitting in separate rooms and deciding if they can still support the dollar while doing so means increasing the risk of loss.

Feb 21, 2005

Soros sees Higher Oil Prices Weakening the Dollar

From CNN/Money:

"The oil exporting countries' central banks ... have been switching out of dollars mainly into euros and Russia also plays an important role in this. That is, I think, at the bottom of the current weakness of the dollar," Soros said.

Soros, dubbed "The Man who broke the Bank of England" for his role as a hedge fund manager in betting the pound would drop in 1992, said he was not predicting further falls in the value of the dollar. But he linked its fate to the price of oil.

"The higher the price of oil the more the dollars there are to be switched to euro (so) the strength of oil will reinforce the weakness of the dollar," he said. "That is only one factor, but I think there is such a relationship."

He also commented on the yield curve.

Soros would not make detailed comments on why long-term borrowing costs have fallen in the face of short-term rate increases, a development U.S. Federal Reserve Chairman Alan Greenspan said on Wednesday he found difficult to explain.

"A flattening of the yield curve is usually an indication of a slowing economy, but here I don't know," Soros said.

Finance Minister and BoJ Clash over Monetary Policy

From the FT,

In testimony to the parliamentary budget committee, Sadakazu Tanigaki, finance minister, said: "If [nominal] interest rates are pulled up now, even by a little, that will cause real interest rates to climb. The Japanese economy can't tolerate that now." Mr Tanigaki said zero rates, though they had unpleasant side effects, had been "underpinning the economy".

Paul Sheard, economist at Lehman Brothers in Tokyo, said Mr Tanigaki's warning about the dangers of premature tightening was a "polite wake up call" to the BoJ. He said talk of tightening either monetary or fiscal policy at a time when the economy had stalled was wrong-headed.

Speculation that the BoJ is preparing to tighten its quantitative easing policy, introduced in March 2001, has risen following the release of minutes showing that two policy board members in December proposed lowering the bank's liquidity target.

Last week, the BoJ left that target unchanged at Y30,000bn-Y35,000bn (US$286bn- $333bn) but analysts will scrutinise minutes of January's policy board meeting, due to be released on Tuesday, to see whether support for lowering the liquidity target has hardened.

Although the BoJ is committed to keeping zero interest rates in place as long as deflation persists, any lowering of the liquidity target would be interpreted by the markets as an prelude to tightening.

How the BoJ reacts to signs of inflation will hopefully be determined by the response of Japanese consumers to inflation. I expect inflation will stimulate the economy making rate hikes and tighter liquidity possible without causing harm to the recovery. This is not an urgent decision though so current policies should be in place another 3-4 months to see how things develop.

Biotech buying

According to the FT($$),

Novartis will launch an agreed tender offer for the balance of Eon Labs shares at $31 a share, a 25 per cent premium over the pre-takeover speculation price of $24.75 a share.I mentioned Eon Labs (ELAB) last week for its technical breakout.

Pop Quiz - Yen

This is from Bloomberg,

Probably an interesting data point though I would write a different headline.

Yen May Fall as Traders Most Bearish in Two MonthsFeb. 21 (Bloomberg) -- The yen is likely to fall against the dollar and the euro as currency traders are the most bearish they've been about the Japanese currency this year, according to a Bloomberg survey of strategists, traders and investors.

Forty-seven percent of the 72 participants polled from Sydney to New York on Feb. 18 advised selling the yen against the dollar, up from 40 percent a week earlier and the most since Dec. 12. Forty-two percent said to sell Japan's currency versus the euro, up from 29 percent.

Lets see on Dec 12th the Yen was... drum roll... 104.79. It then took until Feb 7th for the Yen to fall below the 105.15 low from Dec 9th. If they are even more bearish now does that mean the recent low (106.84) will last at least 3 months?

Probably an interesting data point though I would write a different headline.

Trading Trends in Interest Rates

These are some technical charts applying my interpretation of Stanley Kroll's trading rules to the current rate environment.

Click on a chart to see a larger image!!

It is hard to look at the 30-yr chart and take away anything but ambiguity after the action of the last couple months. With the FOMC committed to avoiding deflation at all costs and Greenspan telling the world last week that he did not really agree with long-term interest rates I lean towards higher rates and have tried to trade that way. The chart no longer supports that view. We also experienced a very whippy broadening range in Dec. (the two most recent highlight marks) leaving little room to benefit from betting either way. Some have mentioned that mortgage hedgers were buying into the most recent highs (price highs yield lows) so maybe it is their negative convexity positions that account for the number of reversals.

Posted by Hello

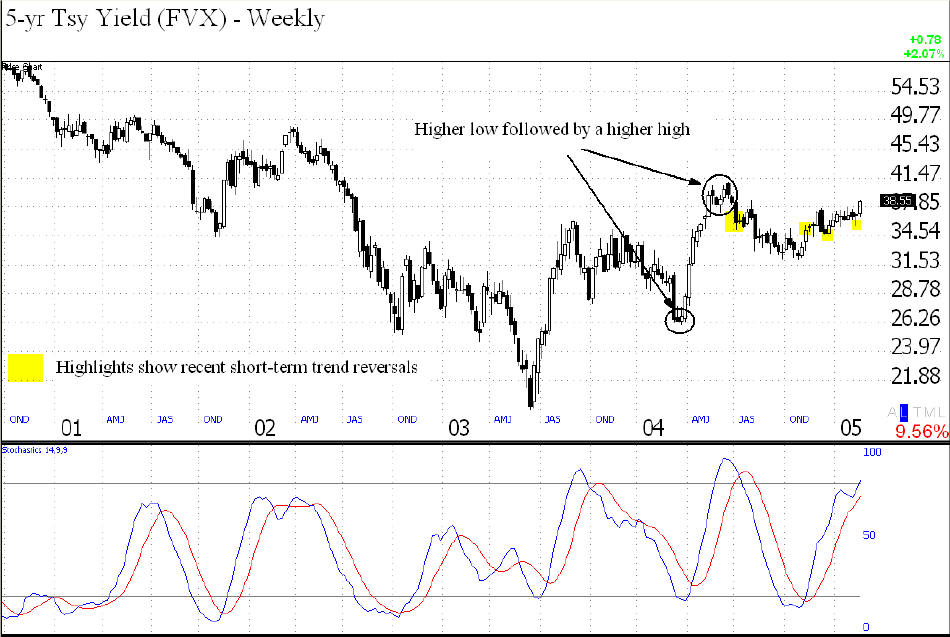

The 5-yr chart shows a much more useful pattern with the yield uptrend looking pretty stable. This reinforces my belief that long rates need to head higher. Trading the 5-yr in here is probably the better option because it allows for tighter stops.

If you read this site a lot you can probably tell that I am a bit obsessed with interest rates. I am mostly interested that a big move may be coming in stocks or bonds because the curve flattening has not coincided with equity weakness. My best guess about the near term is that short yields continue higher and long rates eventually turn to follow within the next 2 months. There is still a strong chance that whatever factors drove long yields to these levels will persist in the near term. Inflation numbers like we had on Friday confirm this view and I would not be too surprised if employment reports begin to show a similar trend towards higher costs. In the short run I think higher rates (and some steepening) will be good for stocks as investors may literally flee the declining bond market to get a piece of corporate profits. Both inflation and higher rates should leave investors with the impression that the economy is stronger than most believe and capable of staying strong even through rate hikes. Over the medium to long term (3-6 months?) stocks will probably come under pressure too as higher rates make bonds more attractive and may uncover some liquidity problems at marginal corporate borrowers.

Oil has a pretty good shot of breaking above $50 next week and if it does a trade through $55 will probably happen within days. That action if it occurs will give a lot of clues to how the markets will react to any impending inflation scare.

It is hard to look at the 30-yr chart and take away anything but ambiguity after the action of the last couple months. With the FOMC committed to avoiding deflation at all costs and Greenspan telling the world last week that he did not really agree with long-term interest rates I lean towards higher rates and have tried to trade that way. The chart no longer supports that view. We also experienced a very whippy broadening range in Dec. (the two most recent highlight marks) leaving little room to benefit from betting either way. Some have mentioned that mortgage hedgers were buying into the most recent highs (price highs yield lows) so maybe it is their negative convexity positions that account for the number of reversals.

Posted by Hello

The 5-yr chart shows a much more useful pattern with the yield uptrend looking pretty stable. This reinforces my belief that long rates need to head higher. Trading the 5-yr in here is probably the better option because it allows for tighter stops.

If you read this site a lot you can probably tell that I am a bit obsessed with interest rates. I am mostly interested that a big move may be coming in stocks or bonds because the curve flattening has not coincided with equity weakness. My best guess about the near term is that short yields continue higher and long rates eventually turn to follow within the next 2 months. There is still a strong chance that whatever factors drove long yields to these levels will persist in the near term. Inflation numbers like we had on Friday confirm this view and I would not be too surprised if employment reports begin to show a similar trend towards higher costs. In the short run I think higher rates (and some steepening) will be good for stocks as investors may literally flee the declining bond market to get a piece of corporate profits. Both inflation and higher rates should leave investors with the impression that the economy is stronger than most believe and capable of staying strong even through rate hikes. Over the medium to long term (3-6 months?) stocks will probably come under pressure too as higher rates make bonds more attractive and may uncover some liquidity problems at marginal corporate borrowers.

Oil has a pretty good shot of breaking above $50 next week and if it does a trade through $55 will probably happen within days. That action if it occurs will give a lot of clues to how the markets will react to any impending inflation scare.

Feb 20, 2005

The Wisdom of Stanley Kroll

In writing Friday about CAO's failure to stop out I got to reading Stanley Kroll's The Professional Commodity Trader looking for a quote about taking stops. I remember something to the effect that if you are going to stop out it is always better to do it sooner rather than later. I couldn't find it but I ran across his rules for trade entry and exit.

I will post a follow up later discussing the current state of interest rates in the context of these rules.

The Professional Commodity Trader by Stanley Kroll is available at Amazon.

I. On Initiating a PositionThat is trading in a nutshell. I absolutely love the footnoted "substantial dangers". Stanley does one of the best jobs I have seen of discussing trading cliches from the perspective of a trader's day-to-day decisions. He treats his own rules the same way. Rules are easy to learn and easy to apply when trades are completed but their correct place at each moment in time is pretty murky.

Trade in the direction of the major tend, against the minor trend. For example if the major trend is clearly up, trade the market from the long side, or not at all, buying when:

a. the minor trend has turned down, and

b. prices are "digging" into support, and

c. the market has made a 35-50 percent retracement of the previous up leg.

If the major trend is clearly down trade the market from the short side, or not at all, selling when:

a. the minor trend has turned up, and

b. prices have advanced into overhead resistance, and

c. the market has made a 35-50 percent retracement of the previous down leg.

II. On Closing Out a Position

a. At a profit. Liquidate one-third of the position at a logical (chart) price objective into overhead resistance (for a long position) or into underlying support (for a short position).*

b. At a loss. There are, basically, three approaches:

* Following this first liquidation, be alert to reinstate the position, or even 1.5 times the liquidated position, on a subsequent technical correction, as outlined in the above discussion, "On Initiating the Position."

- Enter and arbitrary "money" stop-loss; e.g., 40-50 percent of the margin deposit.

- Enter a chart-point stop-loss; i.e., to close out the position when the major trend reverses against your position - not when the minor trend reverses (that's just the point where you should be initiating the position, not closing it out).

- Maintain the position until you are convinced that you are wrong (the major trend has reversed against you) and then close out on the first technical correction.**

** There are substantial dangers to this particular approach, which will be discussed later in the chapter

I will post a follow up later discussing the current state of interest rates in the context of these rules.

The Professional Commodity Trader by Stanley Kroll is available at Amazon.

Feb 18, 2005

We're Number One

In honor of Exxon's (XOM) crowning achievement today here is a site that seems pretty bullish on oil.

That's a pretty interesting group of links on the right and I was generally surprised by how many there are. Maybe its a Michael Moore thing.

That's a pretty interesting group of links on the right and I was generally surprised by how many there are. Maybe its a Michael Moore thing.

CAO's Lesson for Traders

Information about the CAO bankruptcy continues to unfold. The latest news is some good insight into how the world of trading works.

The fact that traders are not normally managing their own capital can also create risk management issues. In the above example it is not clear why a formal request was necessary to close the position but the existence of such a rule makes risk managment difficult because time is such a critical part of loss estimates. In such a situation it seems like a natural stop point has nothing to do with capital availability and needs to occur before the decision gets kicked up the chain of command.

At any rate at some point the loss grows big enough that it becomes more attractive to push it around than to stop the bleeding. That is what is being described above. Jiulin probably could have cut 1/3 or 1/2 of the postion while waiting to here from his bosses. It is the nature of a badly losing position to make its owner believe it will recover. In times like this the market is probably dislocated by the pressure of the position making the recovery all the more likely. Jiulin did not want to stop out at the top of a winning short. On vacation or not his bosses probably did not want to cover either. Now they try to pin the loss on each other. That is how it goes.

Volumes have been written about the need for trader's to manage their emotions but in the real world that is only half of the battle. All large trading operations utilize a chain of command usually with more experienced traders at the top with fewer positions of their own to manage. These senior traders act more to monitor the positions and state of mind of the people beneath them. This system should in effect backstop any trader's personal tendency to let losses run.In an interview with China's state-owned Xinhua news agency, Chen Jiulin blamed the slow response from elusive senior officials at the Beijing-based China Aviation Oil Holding for the escalation of the scandal. Such finger-pointing is rare in China, especially given that the Xinhua agency is widely thought to be supportive of state-owned enterprises.

"When we realised on October 3 that we might incur serious losses, we had a loss of just $80m," Mr Chen was quoted by Xinhua as saying. "If we could get approval from the parent company to clear all positions on that day, the total loss would be less than $100m. But most senior executives [of CAOH] were then on holiday."

He said CAO on Oct 9 submitted to CAOH a formal request to liquidate its holdings, at which moment the actual loss was $180m. But the parent company didn't respond until a week later when it held the first meeting to discuss the crisis. (FT $$)

The fact that traders are not normally managing their own capital can also create risk management issues. In the above example it is not clear why a formal request was necessary to close the position but the existence of such a rule makes risk managment difficult because time is such a critical part of loss estimates. In such a situation it seems like a natural stop point has nothing to do with capital availability and needs to occur before the decision gets kicked up the chain of command.

At any rate at some point the loss grows big enough that it becomes more attractive to push it around than to stop the bleeding. That is what is being described above. Jiulin probably could have cut 1/3 or 1/2 of the postion while waiting to here from his bosses. It is the nature of a badly losing position to make its owner believe it will recover. In times like this the market is probably dislocated by the pressure of the position making the recovery all the more likely. Jiulin did not want to stop out at the top of a winning short. On vacation or not his bosses probably did not want to cover either. Now they try to pin the loss on each other. That is how it goes.

A Fannie Bounce?

As I watch Fannie (FNM) fall here I can't help thinking it will make its way back to $60 for the close. To many long gamma positions with profits to capture if a bounce gets started.

That said if it does make $60 it becomes a pretty compelling short for next week with expirey out of the way.

That said if it does make $60 it becomes a pretty compelling short for next week with expirey out of the way.

Feb 17, 2005

Feb 15, 2005

Bullish

Tonight quite a few stocks show up in good position for long entry. These stood out to me: ARRS, OVTI, RRI, ELAB, AMXC, EXAS, and EDGR. Computer Associates (CA), which had kind of a bad day, appears to have made a reversal off a new low with divergent momentum. If it opens tomorrow with a gap up it would be a good trade against today's low. Otherwise I would hold off for a move up on volume.

I am getting quite a bit more bullish on stocks in here. Partly because of the charts but mostly because of the negative sentiment. The markets have corrected a lot of the damage from January. The Nasdaq which has been underperforming seems to be coloring psychology quite a bit but with the semis looking extremely bullish and the internet stocks looking ready to participate I don't see that index remaining an obstacle for long.

My bullish feelings on stocks leave me a bit mystified about bond yields. I understand the short term dynamic with a strong move higher following the break out of the Q4 range, and as I said last week I would even expect a restest of the new highs. The strength in the commodity sectors and numerous new highs in foreign equity markets just makes a global slowdown seem very unlikely. Without that the Fed will keep going and a 4.40% long bond will look silly. Brad

Also, I apologize for the appearance of the site. Blogger seems to be having some issues so I am having trouble posting and can not get in to take down all the screwed up posts that eventually made it to the site from yesterday. Hopefully I can fix it shortly.

A couple of posts worth checking out are Brad Setser's discussion of why the global imbalances can't last and this article on the slack job market. The latter is so negative it almost feels like a bottom. If inflation does kick up in the next 3 months that may be the case.

I am getting quite a bit more bullish on stocks in here. Partly because of the charts but mostly because of the negative sentiment. The markets have corrected a lot of the damage from January. The Nasdaq which has been underperforming seems to be coloring psychology quite a bit but with the semis looking extremely bullish and the internet stocks looking ready to participate I don't see that index remaining an obstacle for long.

My bullish feelings on stocks leave me a bit mystified about bond yields. I understand the short term dynamic with a strong move higher following the break out of the Q4 range, and as I said last week I would even expect a restest of the new highs. The strength in the commodity sectors and numerous new highs in foreign equity markets just makes a global slowdown seem very unlikely. Without that the Fed will keep going and a 4.40% long bond will look silly. Brad

Also, I apologize for the appearance of the site. Blogger seems to be having some issues so I am having trouble posting and can not get in to take down all the screwed up posts that eventually made it to the site from yesterday. Hopefully I can fix it shortly.

A couple of posts worth checking out are Brad Setser's discussion of why the global imbalances can't last and this article on the slack job market. The latter is so negative it almost feels like a bottom. If inflation does kick up in the next 3 months that may be the case.

Feb 13, 2005

GM - Fiat

According to

the FT ($$),

start of the year, GM appears to be making a base. The next level of

interest looks like the $40 1/2 level.

Click on the chart to see a larger image!!

Posted by Hello

I imagine there is no need to play until it clears resistance and

retests it from above.

Given the impact this story has had on credit spreads the end of the

story could have some broader positive implications. It also looks to

me like Fannie Mae (FNM) could be ready for a short-covering bounce

as it is very oversold and has not managed to get below the $60

level. I don't think it is worth playing as a long but a bounce

towards $66-68 wouldn't surprise me.

the FT ($$),

After the initial weakness at theOn Sunday, Italian newspapers reported that

Fiat and GM were set to announce a settlement to scrap a disputed put

option that would have allowed Fiat to force GM to buy its

loss-making car unit.Papers said GM would pay Fiat about

1.5-1.8 billion euros in cash to cancel the put and change the

structure of a joint venture in engines and platforms in Fiat’s

favour.Nobody at Fiat or GM was immediately available to

comment.

start of the year, GM appears to be making a base. The next level of

interest looks like the $40 1/2 level.

Posted by Hello

I imagine there is no need to play until it clears resistance and

retests it from above.

Given the impact this story has had on credit spreads the end of the

story could have some broader positive implications. It also looks to

me like Fannie Mae (FNM) could be ready for a short-covering bounce

as it is very oversold and has not managed to get below the $60

level. I don't think it is worth playing as a long but a bounce

towards $66-68 wouldn't surprise me.

Feb 12, 2005

New Link

I just added a link to the Capital Chronicle on the right. I corresponded with Alzahr a while back but never ran into his blog until today. He sits in the U.K. and I am resolved to find some more international blogs this weekend.

I generally feel that one of the biggest hurdles U.S. investors face is learning about non-U.S. investments. The global markets are not that isolated but for some reason the brokerage industry has not really caught on to that yet. I imagine a big trend over the next 10 years will be the end of home country bias for U.S. investors.

I generally feel that one of the biggest hurdles U.S. investors face is learning about non-U.S. investments. The global markets are not that isolated but for some reason the brokerage industry has not really caught on to that yet. I imagine a big trend over the next 10 years will be the end of home country bias for U.S. investors.

Feb 11, 2005

Another Week

The equity market got the turn around it needed yesterday morning but the movements in the bond market have really got me scratching my head. I fall pretty squarely into the inflation and dollar worry camp so I have a really hard time seeing why the long end of the yield curve has gotten as low as it has. Yesterday brought a pretty strong reversal there but other than saying that the market woke up to reality I don't really see the cause. If that is indeed the case the long-end has a fair bit of selling ahead of it to get back in line with the rest of the markets.

A few thoughts I have in here:

A few thoughts I have in here:

- The bond market and dollar need to retest their highs while I would not expect commodity markets to challenge their lows.

- I have never really known the Fed to leak a whole lot, but Brad DeLong writes, "The word from inside the Federal Reserve is that Alan Greenspan is *not* optimistic about the dollar and *not* unconcerned about the U.S. budget deficit: that he was trying to express concern without triggering a dollar sell-off: that his words have been misinterpreted by markets as being more optimistic than they were intended to be."

- The strong metal bounce and chorus of strong overseas markets could very quickly swing the pendulum towards inflation fears. With many commodities still nearer multi-year highs than lows there is a very real threat that the U.S will experience cost push inflation inspite of a weak labor market and slack capacity.

- U.S. equities may provide a safe haven from inflation but better real returns will be offered in foreign equity markets.

- Japan looks like it is almost done consolidating its gains from late last year.

Paid Search Bubble?

I just learned that eBay is the largest purchaser of paid search advertising in the world and that they believe current prices are a bit out of whack.

Q. MarketWatch: You've suggested that there is a "bubble" in paid search. This suggests that pricing won't be sustainable. Why is it a bubble? And, can you quantify the rise in paid-search prices eBay is paying?I posted some similar thoughts about this as a comment on Bill Cara's blog. I have never purchased an internet ad or keyword so my comments seemed to have been passed over by the main stream media.A. Bill Cobb: Frankly, we're surprised that keywords have gone as far as they have. Whether it will continue, I don't know. ... We believe we're the largest buyers of keywords in the world. It's our observation that large advertisers, global multinationals are experimenting and not being efficient. Over time they'll get better at this.

Feb 10, 2005

Tough Market to Love

I wonder if we have turned a corner in the market where low interest rates are no longer "good" for stocks. On its own the damage to stocks was not too severe today but it certainly has the potential to get worse quickly. The nasdaq seems particularly weak as we are right back at QQQQ 37 after only one day of selling. We probably need to get a bounce tomorrow morning if the markets wants to keep this rally going to the Dec highs.

One saving grace in here could be the strength in foreign equity markets. Equity markets in Mexico, Brazil, France, and Taiwan don't seem to be experiencing the deflationary doubts of the U.S. The world never moves in perfect synch but it is something to keep an eye on.

One saving grace in here could be the strength in foreign equity markets. Equity markets in Mexico, Brazil, France, and Taiwan don't seem to be experiencing the deflationary doubts of the U.S. The world never moves in perfect synch but it is something to keep an eye on.

Feb 9, 2005

Slow Week

Today is a bit like Monday and Tuesday but slightly more negative. Selling some more this AM. Gradually working towards flat. I don't see much of a reason for a bounce in the afternoon but maybe HPQ and Dell can get something started.

It is difficult to tell whether the emotional indifference should be considered bullish or bearish.

The long end of the bond market is getting some support from the rally in the short end today.

It is difficult to tell whether the emotional indifference should be considered bullish or bearish.

The long end of the bond market is getting some support from the rally in the short end today.

Post on Offsite Meeting

I just put a new post, that has nothing to do with the current state of financial markets, up on my other site if anyone is interested.

Feb 8, 2005

Trimming

Sticking with my plan and making some partial sales but not very much. I would say there is still another leg up in this rally. I am focusing the sales in my losing to flat positions.

I would be very leary of betting against the rally in dollars or bonds. The moves are sharp and probably need to base out for several weeks before turning the other way. Bonds in particular seem like they will target the 4.18 yield lows. Also be aware that bond volatility has increased significantly with this move up.

I would be very leary of betting against the rally in dollars or bonds. The moves are sharp and probably need to base out for several weeks before turning the other way. Bonds in particular seem like they will target the 4.18 yield lows. Also be aware that bond volatility has increased significantly with this move up.

Firefox vs. Internet Explorer

Just flagging the story that Gartner is considering Firefox a serious challenge to IE. No effect for the markets just something I have been watching out of personal interest.

Macro swings

The big news this year is clearly the movement in the dollar, bonds, metals and oil. Equities by comparison are trading mostly flat. Today's latest jump in the dollar is being attributed by most to the new Bush budget. This is a less sanquine view that elminates a lot of the rhetoric from the mainstream reporting.

While I can't really find any fault with that summary, for trading purposes I would set it aside. The markets clearly like something here about the dollar which is creating some broad knock on effects. While the budget may not justify the move now I bet by the time this move is over we will see some actual good news coming out. It looks like maybe 2 months or longer before the weakening dollar / U.S. debt problems will have a shot at reasserting themselves in markets.

One of the difficulties in trading the U.S. equity markets right now is the lack of passion in participants. Most seem willing to chase whatever move is underway and there is very little commitment by bulls or bears to a longer-term view. This may be due in part to the dollar volatility which makes it very difficult to predict where earnings and equity values will go. At any rate it makes it difficult for the market to create a lasting trend. This is absolutely not so for the dollar, gold, oil and other macro variables. Everyone has an opinion and even the viscious moves we are seeing now do not seem to be causing many side changes. I am pretty sure I spent January a bit caught up in my view too and am going to step back a bit to evaluate things from a longer term perspective.

The dishonesty of the administration about budget deficits has reached levels unheard of. These folks have absolutely no shame. Bush presented today a budget that claims that he will achieve his goal of reducing the deficit by half by 2008 (from a false 2004 baseline of $521 billion rather than the actual 2004 deficit of $412b) and will achieve a deficit of "only" $233b by 2009. Even better news, the administration claims today: the "halving" of the deficit will be reached by 2008, a year earlier than original 2009 target for it.

Who are these accounting scam artists trying to deceive? Do they think everyone in America and around the world is a mathematically challenged total idiot or an accounting moron?

The reality is, that based on realistic scenarios outlined last week by the non-partisan Congressional Budget Office, the deficit by 2009 will be close to $600b (or 4.0% of GDP) rather than falling to $233b; and the deficit will reach over $1,100b (or 5.5% of GDP) by 2015. (continue reading)

While I can't really find any fault with that summary, for trading purposes I would set it aside. The markets clearly like something here about the dollar which is creating some broad knock on effects. While the budget may not justify the move now I bet by the time this move is over we will see some actual good news coming out. It looks like maybe 2 months or longer before the weakening dollar / U.S. debt problems will have a shot at reasserting themselves in markets.

One of the difficulties in trading the U.S. equity markets right now is the lack of passion in participants. Most seem willing to chase whatever move is underway and there is very little commitment by bulls or bears to a longer-term view. This may be due in part to the dollar volatility which makes it very difficult to predict where earnings and equity values will go. At any rate it makes it difficult for the market to create a lasting trend. This is absolutely not so for the dollar, gold, oil and other macro variables. Everyone has an opinion and even the viscious moves we are seeing now do not seem to be causing many side changes. I am pretty sure I spent January a bit caught up in my view too and am going to step back a bit to evaluate things from a longer term perspective.

Housing article

Minyanville brought this article on housing speculation to my attention today. There has obviously been a ton of stuff written about the housing market and by now I would guess everyone has chosen sides about whether we are in a bubble or not. I just wonder how many people that are buying houses really know how the market is managed by the building / development companies.

At any rate, the influence that the sellers have on price should make everyone question exactly what the risk is in the house. Most people equate price volatility with risk but to do so in this case could be pretty deceptive.

At any rate, the influence that the sellers have on price should make everyone question exactly what the risk is in the house. Most people equate price volatility with risk but to do so in this case could be pretty deceptive.

Trains can't catch you...

Tried to go through the charts and not read too much into them on a slow day. The only thing that stood out to me was that lots of communication and communication equipment stocks showed up in bullish scans. Makes a lot of sense because the mergers in the sector show that big players have money and also that consolidation (and a return to profitability) is under way.

In the semi sector PMC Sierra stands out by being in a good position to rally.

Commodities look like they are in for a bit of pain as the dollar and bond rally could lead to a deflation scare. Gold and silver are already in the dumps while other sectors like the oil stocks are making highs. Alcoa (AA) looks like it may have put in a bottom so maybe the markets are just sorting out the commidities a bit. Until the dollar and bonds can make tops the space is probably pretty risky.

In the semi sector PMC Sierra stands out by being in a good position to rally.

Commodities look like they are in for a bit of pain as the dollar and bond rally could lead to a deflation scare. Gold and silver are already in the dumps while other sectors like the oil stocks are making highs. Alcoa (AA) looks like it may have put in a bottom so maybe the markets are just sorting out the commidities a bit. Until the dollar and bonds can make tops the space is probably pretty risky.

Feb 7, 2005

Green Light

Friday's afternoon march higher seems to have given the green light to everyone that became hesitant during the January selloff. Today and tomorrow should show a strong positive bias but the question will be what sort of volume is drawn into the market. My guess is that returns get a bit harder after that and the market may begin a topping process. The best way to play until maybe next Friday could be by looking for sector rotations. The internet sector stand out a bit for its recent weakness while Google (GOOG) has easily held 200. I would not be surprise if that sector attracts some capital.

I will probably try to sit on my hands today, make some sales tomorrow afternoon, and then begin running a flatter book. We'll see how it goes.

I will probably try to sit on my hands today, make some sales tomorrow afternoon, and then begin running a flatter book. We'll see how it goes.

Feb 6, 2005

Blood from a Stone

Friday's trading had two significant breakdowns, the yield on the long bond left 4.60% in the dust and the VXO closed below 11%. Both these moves are symptomatic of the chase for returns that is underway.

Click on the chart to see a larger image!!

Posted by Hello

Normally treasury yields and equity volatilities are inversely correllated and you can even see the inverse correlation happening over short periods during the last year while the trend in both has been lower. I expect that positive relationship between volatilities and yields may last for a while as they are both related to excessive investment in U.S. assets.

The financial times explained the bullish move in bonds (U.K. gilts and global rates) like this:

I don't believe there is a shortage of available infrastructure investment that could be made in the developing world. I tend to see policy moves like the G7 decision to forgive developing country debt as indications that the G7 governments "get it" and are forcing liquidity out to the perifery where it can be put to better use.

Posted by Hello

Normally treasury yields and equity volatilities are inversely correllated and you can even see the inverse correlation happening over short periods during the last year while the trend in both has been lower. I expect that positive relationship between volatilities and yields may last for a while as they are both related to excessive investment in U.S. assets.

The financial times explained the bullish move in bonds (U.K. gilts and global rates) like this:

The lack of good investment alternatives is also creating an excess of money fighting for short term gains in financial markets pressing volitilities towards historic lows. I would guess that trend did not end on Friday but that it may end within the next few months. It is a good explanation of what is going on in the short run but I doubt this situation can persist.Yet there may be a more elementary explanation for low long-term real interest rates. Just as the price of bananas balances the supply and demand for this fruit, so the rate of interest balances the supply of savings against the demand for funds to invest. Monetary policy is important mainly at the short end and for its effect on inflation. But the important influence at the longer end is the balance of world savings and investment.

Thus, I come to the simple hypothesis that falling real interest rates reflect a growing shortage of attractive investment projects to absorb savings. The world is indeed supposed to be short of capital and we are told that we do not save enough. But what matters in this context is not the developing world projects that might be desirable but the number of projects world-wide that promise a commercial risk-adjusted return.

The reason why so much of the world's savings has gone to the US is surely just because of the dearth of such investment outlets elsewhere. In the 1930s, Lord Keynes feared that the rate of interest could not fall low enough to balance savings and investment at a reasonable level of employment. But up to now, world capital markets have worked well and interest rates have fallen enough to balance savings and investment without generating a depression.

I don't believe there is a shortage of available infrastructure investment that could be made in the developing world. I tend to see policy moves like the G7 decision to forgive developing country debt as indications that the G7 governments "get it" and are forcing liquidity out to the perifery where it can be put to better use.

Feb 4, 2005

Disconnect

I mentioned a disconnect between the Fed and the bond market regarding inflation. This disconnect was reflected in Greenspan's speech this AM.

The willingness of European companies to accept lower profits in the US over the past three years as the dollar has declined helped prevent inflation rising in the US, Mr Greenspan said. But he held out the prospect that import prices might soon be on the rise. Peter Hooper, chief US economist at Deutsche Bank and a former top official at the Fed, said: "The main implication is that the Fed is not quite so sanguine on inflation pass-through from the dollar as we might have been led to believe."

Clickety

Kla-Tencor (KLAC) is fast approaching the $49 area. Taking some off the table makes sense I imagine. Maybe Texas Instruments (TXN) can continue to pull the train but those are pretty big moves today and may need to consolidate.

General Electric (GE) might have a shot at a long side trade here. Has a nice base for a stop.

Also, I chucked some steel stocks off the ship as they have had a good run. Copper stocks are being pulled down by Phelps Dodge (PD) and US Steel (X) has flagging momentum at highs. Those thoughts and today's bond action makes me wonder if they can head higher.

General Electric (GE) might have a shot at a long side trade here. Has a nice base for a stop.

Also, I chucked some steel stocks off the ship as they have had a good run. Copper stocks are being pulled down by Phelps Dodge (PD) and US Steel (X) has flagging momentum at highs. Those thoughts and today's bond action makes me wonder if they can head higher.

Yeah But...

The tape is gliding higher and lots of momentum patterns are managing to add to gains. Something does not feel quite right to me though. Maybe the market is just experiencing anxiety over the bad jobs report but there does not seem to be a great deal of volume associated with the price climbs. Take a look at Intel (INTC) for example. Anemic. Also, I am not noticing many new stocks breaking bases to create the next wave of advancers. I am trying to sit on my hands here and just roll up stops.

One more thought, if the jobs numbers created a deflation scare wouldn't the Euro appreciate like crazy? Unlike the U.S. and Japan, the ECB has been unwilling to print currency in an effort to spur growth so I am not sure how deflation makes the Euro weaken.

I gave my little tirade about the slack jobs market this AM but this guy really digs into the numbers. And while I am back on the subject, today's labor report seemed pretty much in line with other recent reports so in my view it was really the distortion of expectations that stands out. Maybe we get a reflex action the other way next month with predictions well below the announced number.

One more thought, if the jobs numbers created a deflation scare wouldn't the Euro appreciate like crazy? Unlike the U.S. and Japan, the ECB has been unwilling to print currency in an effort to spur growth so I am not sure how deflation makes the Euro weaken.

I gave my little tirade about the slack jobs market this AM but this guy really digs into the numbers. And while I am back on the subject, today's labor report seemed pretty much in line with other recent reports so in my view it was really the distortion of expectations that stands out. Maybe we get a reflex action the other way next month with predictions well below the announced number.

Stop That!

If I turn and look up from here, allowing myself to squint a bit, I can actually see the stop levels on my long bond trade. Clearly there is a disconnect between what I see and what the market sees. I also would say there is a bit of a gulf between the Fed's view that o/n rates are accomadative and the long bond's view that the gov't has run out of paper to print bonds on.

While I'm at it does anyone out there really believe that the unemployment rate is improving. I am going to go out on a limb and say that some day economists will look back at this period and realize lots of people could not admit they did not have jobs.

No more bond shorts until we make it back above 4.57 yield.

While I'm at it does anyone out there really believe that the unemployment rate is improving. I am going to go out on a limb and say that some day economists will look back at this period and realize lots of people could not admit they did not have jobs.

No more bond shorts until we make it back above 4.57 yield.

Back to Plan A

The Yen move lower now appears to be a headfake as it moved comfortably back into the pennant. Other currencies are still heading lower against the dollar and that has brought my attention back to those cross rates. I am going to be patient on my entries and look to short GBP / Yen again above 196. I am also looking at Euro / Yen for a short above 135.5. That will probably be it until late next week.

Here is summary of the overnight chatter causing the move. The GBP strength is being attibuted to a particular difference between British and U.S. opinions over debt forgiveness.

Here is summary of the overnight chatter causing the move. The GBP strength is being attibuted to a particular difference between British and U.S. opinions over debt forgiveness.

China vs. India

While outsourcing as a news topic seems to have come and gone with the election, it is still alive and well as an industry.

Of China's 8,000-some software services providers, only five have more than 2,000 employees, the firm said in its first 2005 McKinsey Quarterly report.

India, by contrast, has fewer than 3,000 software services companies, McKinsey said. At least 15 of these have more than 2,000 workers, and some--including Infosys Technologies, Tata Consultancy Services and Wipro Technologies--have "garnered international recognition and a global clientele," McKinsey said.

Although revenue from information technology services is rising in China, it is barely half of India's $12.7 billion a year, McKinsey said.

I have mixed feelings about what the impact of outsourcing has really been but given the $9 trillion U.S. GDP the above numbers look a bit insignificant. These numbers exclude subsidiaries but even if that is 90% of the job shift the total impact is only around $190 bln.

Feb 3, 2005

The January Effect

Now that January is over it seems some investors are stepping up to the plate.

Typically the strong period goes to mid-March. If the markets continue higher I would be looking for signs of distribution. The pullback that started in January had some teeth to it so I don't think the market can hop back off to the races without doing some work below the Dec highs.Investors poured an estimated $3.6 billion into U.S. and international stock mutual-funds in the week through Feb. 2, the fastest pace since mid-December, data provider TrimTabs Investment Research reported Thursday.

U.S. stock funds realized net inflows of $2.8 billion, compared to outflows of $747 million the prior week.

Meanwhile, investors sent $872 million to international equity funds, following additions of $1.5 billion a week earlier.

Bond funds saw inflows of $653 million, reversing outflows of $302 million the prior week, while hybrid funds -- which buy stocks and bonds -- had inflows of $661 million vs. inflows of $562 million the week before.

Separately, TrimTabs reported that about $500 million was pulled from Exchange Traded Funds that track U.S. stock indexes during the week, compared to an inflow of $2.2 billion the prior week.

The Dressing Room

The leadership if there is any is coming from retail and particularly the teenage apparel sellers. Abercrombie & Fitch (ANF) got the ball rolling with its numbers but is now pulling Urban Outfitters (URBN), American Eagle (AEOS), and Quicksilver (ZQK) along on the ride. While its cloths are not as trendy, the Gap (GPS) stock has a very sassy looking short term pattern going so maybe it will hop in on the rally too.

Was probably a better trade for the morning but I mentioned these stocks a while back so I am flagging them again.

It is difficult to see how this fits into the global inflation or deflation picture other than to say that certainly the mall shopping portion of the population has money.

Was probably a better trade for the morning but I mentioned these stocks a while back so I am flagging them again.

It is difficult to see how this fits into the global inflation or deflation picture other than to say that certainly the mall shopping portion of the population has money.

UST Supply Shortage

Brad Setser has an interesting post on the effect of treasury issuance on the shape of the yield curve.